{kind=link}

01 May 2026 – The first quarter of 2026 delivered a useful reminder that not all online advertising growth is created equal. Meta outpaced WARC Media’s forecast, while Amazon held steady, and YouTube continued to struggle even as Alphabet’s wider advertising machine powered ahead.

This is according to analysis by WARC Media in its latest Earning Debrief, an advertising revenue performance analysis of Big Tech compared against WARC Media’s quarterly global ad spend forecast data, to provide a current round-up of their ad spend.

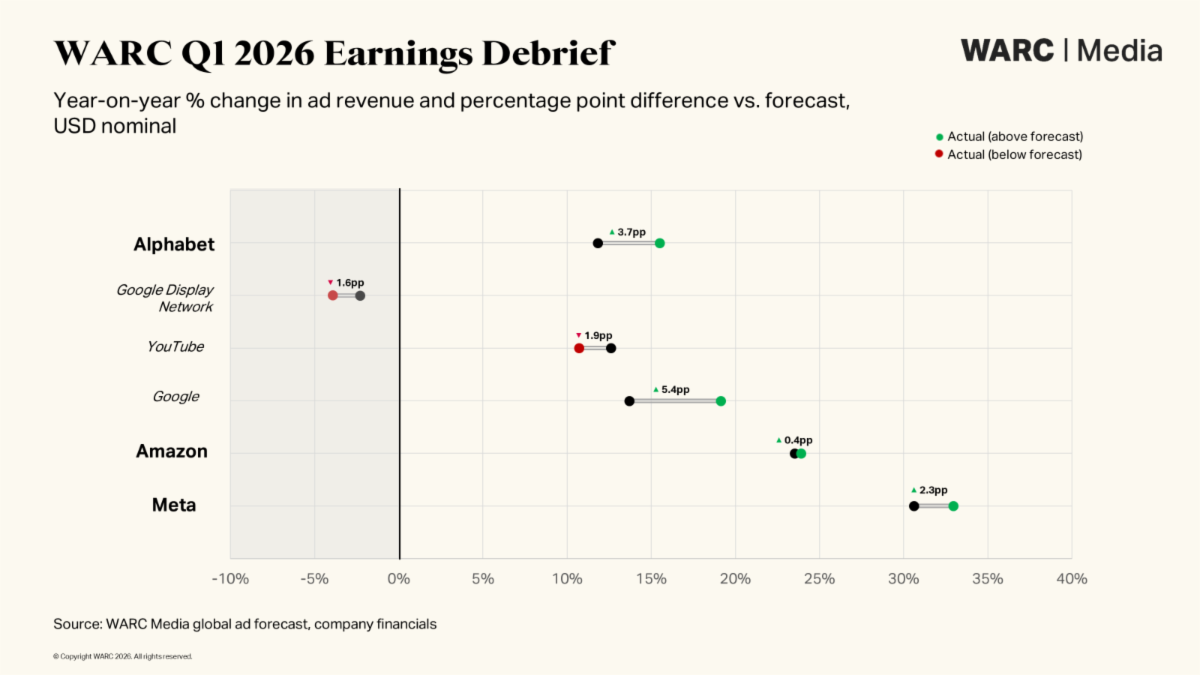

Benchmarking against WARC Media’s ad spend projections – derived from a proprietary neural network of over two million data points – Meta’s reported growth beat expectations by 2.3 percentage points (pp) during the opening quarter of 2026. Google Search outperformed by 5.4pp, and Amazon’s ad business came in broadly level (-0.4pp). YouTube, however, once again fell short of projections (-1.9pp), while Google’s Display Network recorded a sharper-than-expected decline (-1.6pp).

James McDonald, Director of Data, Intelligence & Forecasting at WARC, said “With this earnings cycle closely tracking our forecasts, WARC’s outlook for the year remains broadly unchanged for the major online platforms. The next phase of growth is likely to favour those that can turn AI from a fashionable noun into a measurable commercial advantage. As ever in advertising, rhetoric is plentiful; revenue is indelible.”

Meta defies gravity

Meta was an overperformer this quarter, with ad revenue of $55.0bn against a forecast of $54.1bn – 2.3pp ahead of WARC’s benchmark. Better targeting, more automated buying and faster optimisation appear to be helping Meta convert its AI infrastructure into measurable performance, rather than merely an expensive slide in an investor deck.

Management commentary reinforces this interpretation. CFO Susan Li reported that ranking improvements on Instagram drove a 10% lift in time spent with Reels in Q1, while Mark Zuckerberg pointed to strong trends across Meta’s apps and all-time high engagement around video content.

The results suggest Meta is increasingly effective at capturing user attention, selling it, monetising it, and commanding premium rates in the process.

Amazon’s full-funnel evolution

Amazon’s advertising services revenue of $17.2bn was effectively in line with first quarter expectations. The world’s largest advertiser is working to be “the best place for brands of all sizes to grow their businesses” and emphasised its full-funnel credentials during its earnings call.

Beyond the messaging, Amazon’s advertising business continues to benefit from the attibutes marketers most value: purchase intent, closed-loop measurement and inventory that sits tantilisingly close to the transaction.

The direction of travel, therefore, remains favourable for Amazon. Retail media continues to gain market share by offering advertisers the alluring prospect of linking spend to sales with minimal attribution complexity, while streaming inventory and AI-assisted creative tools broaden Amazon’s reach beyond the lower funnel. This bodes well for future earnings cycles.

Alphabet’s mixed quarter

Google was the standout performer during the quarter, with ad revenue up 19.1% to $60.4bn, a marked 5.4pp above the benchmark of +13.7%. Clearly traditional paid search remains resilient, and Alphabet is arguing with some confidence that AI is improving engagement rather than cannibalising it.

Indeed, CEO Sundar Pichai heralded that AI is “illuminating every aspect of the business” and that products such as AI Overviews and AI Mode are now bringing users back to search more often. While progress is evident, the quarter revealed uneven performance across Alphabet’s advertising portfolio, with AI-driven gains not distributed equally among all business units.

YouTube’s reported ad revenue of approximately $9.98bn came in around $72m below the forecast value of $10.05bn, suggesting that strong engagement is still not converting into revenue quite as elegantly as executives would prefer. Short-form video continues to attract attention at scale, but monetisation still appears to lag the consumption curve: this is now the second consecutive quarter in which YouTube has fallen short of WARC’s forecast expectations, though the gap was far wider last quarter.

Google’s Display Network continues to decline in step with a moribund open web. Here, ad revenue dipped 3.9% compared to a forecast fall of 2.3% – this suggests Alphabet’s AI ambitions may be creating trade-offs in certain areas potentially at the expense of others.

Final word

Given the combined scale of these three players – accounting for 58% of all ad investment globally excluding China – they provide a useful yardstick for the industry at large.

The pace of growth at Amazon by far exceeds the WARC Media forecast for Q1 2026 ad spend on retail media globally (+12.3%); ditto Meta in relation to WARC’s benchmark for social media in the quarter (+20.3%). And that without looking at forecasts for slower-growth channels like total TV (+1.2%), or the market as a whole (+11.1%).

Taken together, the quarter suggests that advertisers are continuing to reward platforms that combine scale, first-party data and increasingly competent automation.

Meta is showing what happens when AI improves both engagement and monetisation simultaneously, Amazon is extending retail media into something closer to a full-spectrum ad business, and Alphabet is proving that search remains formidable even as video and display raise less cheerful questions